JSE-listed Aspen Pharmacare Holdings Limited (APN), a global multinational specialty pharmaceutical company, has reported solid Group financial results for the year ended 30 June 2024.

Stephen Saad, Aspen Group Chief Executive said, “We delivered our highest ever six-month normalised EBITDA in H2 2024 growing 17% over H1 2024 and building momentum for sustainable growth. Manufacturing revenue grew by 25% led by finished dose form revenue up by 33% with Commercial Pharmaceuticals growing 4% after absorbing the impact of volume-based procurement (“VBP”) in China. Regionally concluded acquisitions in China and Latin America contributed to derisking the base Commercial Pharmaceuticals business which is well poised for future growth. Robust cash generation from earnings was underpinned by sustainably lower working capital investment, assisted by the recently announced change in the operating model of our Heparin business which released R2,9 billion in inventory.”

“Our pursuit of manufacturing and commercial opportunities to enter the rapidly growing GLP-1 market for breakthrough products in the treatment of diabetes and obesity has advanced positively. This exciting opportunity could benefit Aspen from calendar year 2026 onwards.”

GROUP HIGHLIGHTS

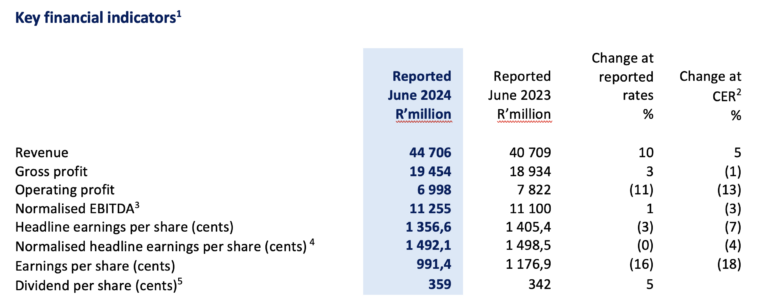

- Revenue increased by 10% (+5% in constant exchange rate (“CER”)) to R44,7 billion (FY 2023: R40,7 billion);

- Normalised EBITDA increased by 1% (-3% in CER) to R11,3 billion (FY 2023: R11,1 billion);

- Normalised headline earnings per share remained flat (-4% in CER) to 1 492,1 cents (FY 2023: 1 498,5 cents);

- Headline earnings per share decreased by 3% (-7% in CER) to 1 356,6 cents (FY 2023: 1 405,4 cents)

- Earnings per share decreased by 16% (-18% in CER) to 991,4 cents (FY 2023: 1 176,9 cents);

- Operating cash flow per share increased 13% to 1 401,4 cents (FY 2023: 1 242,6 cents);

- Dividend declared to shareholders increased by 5% to 359 cents per ordinary share (FY 2023: 342 cents).

1 The Group assesses its operational performance using constant exchange rates (“CER”). The table above compares performance to the prior comparable period at reported exchange rates and at CER.

2 The CER % change is based upon the performance for the year ended 30 June 2023 recalculated using the average exchange rates for the year ended 30 June 2024.

3 Operating profit before depreciation and amortisation adjusted for specific non-trading items as defined in the Group’s accounting policy.

4 Normalised headline earnings per share (“NHEPS”) is headline earnings per share (“HEPS”) adjusted for specific non-trading items as defined in the Group’s accounting policy.

5 Dividend declared on 2 September 2024, to be paid on 23 September 2024 (2023: Declared on 29 August 2023 and paid 26 September 2023).

GROUP PERFORMANCE

H2 2024 was the start of Aspen’s journey to both realising the tangible benefits from sterile manufacturing investments and the delivery of a predictable, resilient, growing Commercial Pharmaceuticals business that has managed and absorbed the volume-based procurement (“VBP”) risks in China. In FY 2024 the Group has achieved a record H2 normalised EBITDA of R6 061 million up 17% on H1 2024. The higher than anticipated negative impact of VBP resulted in Aspen falling short of its targeted mid-single digit growth in EBITDA.

Group Revenue for the reporting period was up 10% led by Manufacturing growing by 25% and Commercial Pharmaceuticals increasing by 4%. Gross Profit grew 3% diluted by an increased Manufacturing sales mix with the primary driver being the liquidation of Heparin inventory of R2,9 billion. Normalised EBITDA of R11 255 million was up 1%.

Net financing costs of R1 232 million (R1 284 million adjusted for capital raising fees on transactions of R52 million) remained flat compared to the prior financial year. Increased net interest costs, fueled by higher rates and increased net debt levels, were offset by lower foreign exchange losses resulting from reduced volatility in emerging market currencies relative to the Euro. Financing costs in FY 2025 will continue to be influenced by the interest rate cycle and currency volatility. NHEPS of 1 492 cents ended marginally below FY 2023. HEPS declined by 3% and earnings per share ended 16% lower affected by higher acquisition related transaction costs and the impairment of VBP impacted intangible assets respectively.

Operating cash flow per share of 1 401 cents grew 13%, supported by an improved operating cash conversion rate of 103% (FY 2023: 88%). This exceeded our internal benchmark of 100%. Solid operating cash flows, even after partial funding of the Latin American product portfolio acquisition of R2,1 billion, coupled with the benefit of reducing the Group’s investment in Heparin inventory by R2,9 billion were the key catalysts in this positive shift. Net debt increased from R22,2 billion in June 2023 to R26,9 billion in June 2024 with net acquisitions totalling R7,7 billion being key to the rise. The leverage ratio ended at 2,3x comfortably within the Group’s targeted range.

SEGMENTAL PERFORMANCE

Commercial Pharmaceuticals

Commercial Pharmaceuticals revenue grew by 4% to R30 570 million with the growth in Prescription and OTC more than offsetting the decline in Injectables revenue. Gross profit margins were marginally lower at 59,4% (FY 2023: 60,0%) after absorbing the impact of VBP in China.

Prescription

Prescription Brands enjoyed double digit growth of 15%, recording revenue of R11 380 million. The revenue growth was underpinned by solid organic growth in its largest region, Africa Middle East, and organic and acquisitive growth in the Americas which is now the second largest region.

Gross profit percentage was up at 60,9% (FY 2023: 60,7%) with favourable sales mix more than offsetting the impact of the regulated price cuts in Australia.

OTC

OTC, the second largest segment in Commercial Pharmaceuticals, grew revenue by 7% to R9 706 million with all regions reporting solid growth. Gross profit percentage of 58,7% remained in line with the prior year of 58,6%.

Injectables

Injectables was impacted by the more severe than expected outcome of VBP in China on Fraxiparine and Diprivan. Growth in Africa Middle East and the Americas (most notably Brazil) partly mitigated the overall segment sales reduction which recorded a revenue decline of 9% to R9 484 million.

Gross profit percentage declined to 58,2% (FY 2023: 60,6%) influenced by the impact of VBP, partly offset by cost of goods savings from the continuing insourcing of sterile production.

Manufacturing

Manufacturing revenue grew significantly, increasing 25% partly aided by exchange rate tailwinds. FDF revenue growth accelerated from 10% in H1 2024 to 33% at year-end, supported by an increased contribution in H2 2024 from third-party contracts for sterile manufacturing. Heparin revenue growth of R1 469 million over the comparable period was largely due to the transition to toll manufacture. API sales were up 2%, following a rebound in H1 2024.

Gross profit of R1 307 million was 2% ahead of FY 2023. The gross profit percentage ended lower at 9,2% (FY 2023: 11,4%) influenced by the increased sales mix of Heparin and the non-recurrence of the grant funding enjoyed in the prior year.

PROSPECTS

The Group has achieved a solid set of results for the year ended 30 June 2024 even after absorbing the more severe impact of VBP in China. The 17% growth in normalised EBITDA in H2 2024 compared to H1 2024 sets a firm foundation in building momentum for anticipated strong growth in FY 2025.

The Commercial Pharmaceuticals business has been derisked and is well poised for future growth. We anticipate Commercial Pharmaceuticals will achieve double digit CER revenue growth in FY 2025 supported by underlying growth in all three business segments and underpinned by organic growth accompanied by annualised growth from recent portfolio acquisitions.

For Manufacturing, we expect FDF, supported by an increased sterile capacity fill contribution, to be the main contributor to CER EBITDA growth in FY 2025. Over the period FY 2025 to FY 2026 (compared to FY 2024) we estimate CER EBITDA to increase incrementally by R2 450 million from these initiatives. This value growth is consistent with previous guidance, but the realisation may vary between the two financial years, dependant on the timing of the South African regulatory approvals.

Supporting our capacity fill and commercial initiatives, Aspen has also secured a commercial license for the intellectual property necessary to commercialise GLP-1s post the expiry of the originator product patents. In addition, Aspen will be the exclusive global supplier of these products to the licensor. This exciting opportunity could benefit Aspen from calendar year 2026 onwards and consequently also be additive to the capacity fill contributions for FY 2026.

Finance costs will continue to be influenced by the interest rate cycle. We are expecting an increase in net interest costs driven by the residual impact of current higher interest rates being carried forward to FY 2025. We expect the effective tax rate to increase in FY 2025 as the profit contribution from sterile manufacturing increases. Lower working capital investment and strong operating cash flows should assist us in achieving an operating cash conversion rate greater than our target of 100%.

Any forecast information in the above-mentioned paragraphs has not been reviewed or reported on by the Group’s auditors and is the responsibility of the directors. The full announcement has been released on SENS and is available on Aspen’s website. Any investment decision must be based on the information contained in the full announcement.

The post Aspen’s revenue increases 10% underpinned by a strong second half performance appeared first on Aspen Pharmacare.